Personal Finances 1

budgeting tips, building an emergency fund, building savings, debt prevention, emergency fund, emergency savings, emergency savings plan, essential expenses, financial goals, financial peace of mind, financial planning, financial preparedness, financial security, financial stability, how to create an emergency fund, money management, personal finance, saving for emergencies, saving money, saving tips

Tayrine Campos

7 months ago

0 Comments

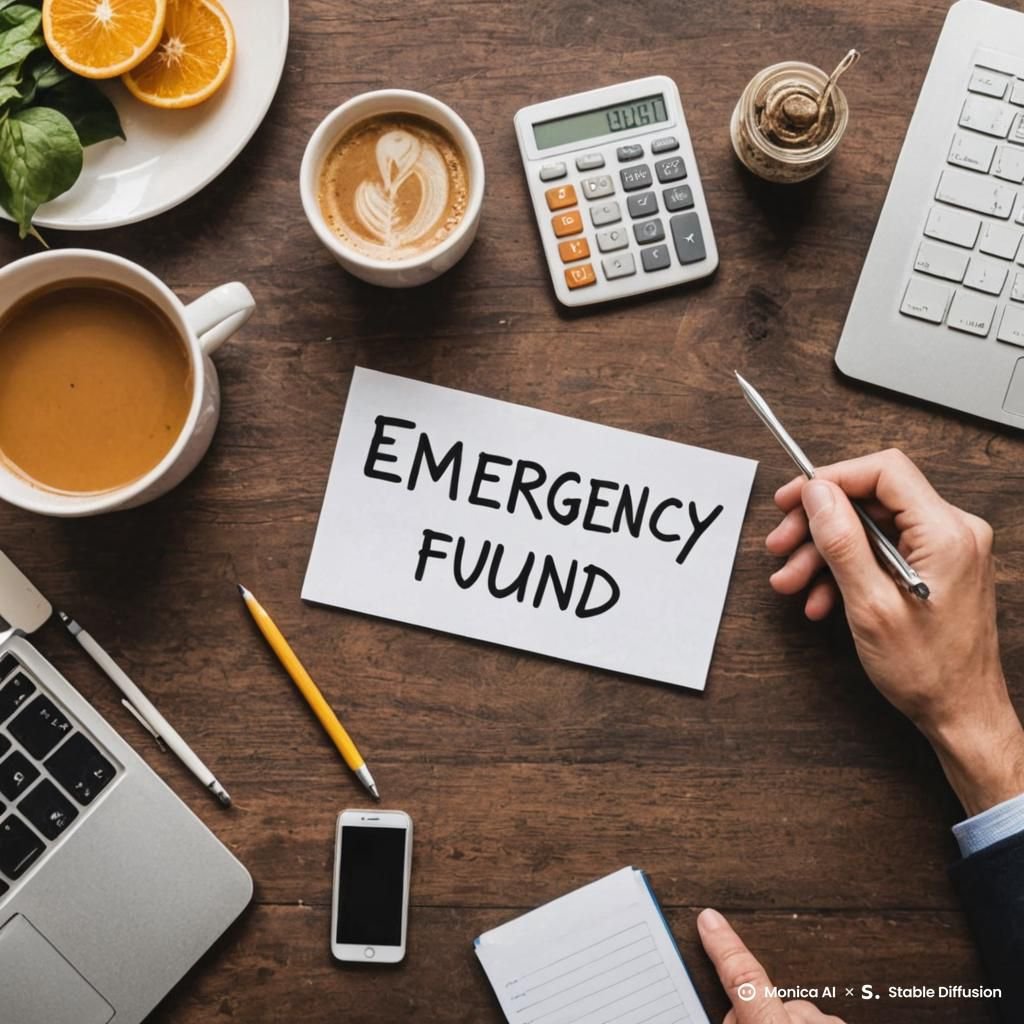

The Importance of an Emergency Fund and How to Create One: A Complete Guide 2025

Having an emergency fund is one of the most important financial practices to ensure stability and security in your life. Often, we face unexpected situations such as job loss, unforeseen medical expenses, or urgent repairs at home. An emergency fund can be the key to overcoming these challenges without resorting to loans or debt. In this post, we will explore the importance of an emergency fund and the steps to create a solid fund that will provide you with greater financial peace of mind.

1. What is an Emergency Fund?

An emergency fund is a financial reserve intended to cover unexpected and urgent expenses such as illness, an accident, job loss, or issues with your car or home. This fund should not be used for regular expenses or luxuries, but rather for emergency situations that may jeopardize your financial well-being.

Why have an emergency fund?

Life is full of surprises, and while it’s impossible to predict exactly what will happen, you can prepare for unexpected events. Without an emergency fund, many people turn to loans, credit cards, or even sell valuable assets to cover these expenses. However, these alternatives often result in accumulating debt and further financial complications.

An emergency fund provides a safety net, allowing you to face financial challenges without the risk of falling into a cycle of debt. It helps reduce financial stress and enables you to focus on finding solutions to your problems without worrying about the financial consequences.

2. What is the Ideal Amount for an Emergency Fund?

One of the most common questions when it comes to emergency funds is how much money should be saved. The answer varies based on individual situations, but experts recommend having enough funds to cover three to six months of essential expenses.

How to calculate the ideal amount?

To calculate the amount you need for your emergency fund, follow these steps:

- List your essential monthly expenses: Include rent, utility bills, groceries, transportation, medications, and any other expenses that are necessary for your daily living.

- Multiply by three or six months: If your financial situation is more uncertain or your job offers little security, it’s more advisable to have an emergency fund that covers six months of expenses. Otherwise, three months might suffice.

For example, if your essential monthly expenses are $3,000, your emergency fund should range from $9,000 to $18,000, depending on your financial situation.

3. Where to Keep Your Emergency Fund?

One of the most important questions when creating an emergency fund is where to keep it. The ideal location should be easily accessible in case of emergency but should also protect the money from being used for non-essential purposes.

Options for keeping your emergency fund:

- Savings account: A savings account is a popular option because it’s easy to access and offers immediate liquidity. However, it provides low returns. Still, it’s a good starting point for those just beginning to build their fund.

- Separate checking account: Some people prefer to create a separate checking account exclusively for their emergency fund. This helps keep the money out of temptation.

- Low-risk investments: For those who already have a substantial amount in the fund and want to earn better returns, a low-risk option such as Treasury bills (T-bills) or certificates of deposit (CDs) could be a good choice. These investments offer security and higher returns than a savings account.

The main recommendation is to choose a place that is easy to access without too much complexity and allows for quick withdrawals when necessary.

4. How to Start Building Your Emergency Fund?

Now that you understand the importance and definition of an emergency fund, it’s time to start building yours. Even if the ideal amount seems high, it’s possible to start small and gradually increase the fund over time.

Steps to build your emergency fund:

- Set a clear goal: Define how much you want to save and within what timeframe. For example, if you want $9,000 in six months, you’ll need to save $1,500 per month.

- Create a financial plan: Adjust your budget so that part of your income is directed towards the emergency fund every month. Consider cutting unnecessary expenses such as dining out, impulse purchases, or unused subscriptions.

- Make regular deposits: Treat the emergency fund as a priority. Every month, make a fixed deposit until you reach the goal you’ve set. This helps you stay disciplined and avoid forgetting to save.

- Review your goal periodically: As your financial life changes, you may need to adjust the amount of your emergency fund. This could happen due to increased expenses or changes in your financial needs.

5. Tips for Maintaining Your Emergency Fund

Having an emergency fund is just the first step. Maintaining and protecting this fund is equally important. Here are some essential tips to ensure you continue to be financially secure.

How to maintain your emergency fund:

- Don’t use the fund for non-emergency expenses: The emergency fund should only be used for true emergencies. Avoid using it for unnecessary purchases, such as a vacation or a new phone.

- Review your fund annually: Your expenses may change over time, so make sure to review your emergency fund at least once a year to ensure it’s adequate for your needs.

- Add to the fund when possible: If you receive a bonus, salary increase, or extra income, consider adding part of this to your emergency fund. This can accelerate the saving process.

6. Common Mistakes When Building an Emergency Fund

Although the idea of having an emergency fund seems straightforward, many people make mistakes when trying to build one. Avoiding these mistakes can make a big difference in the success of your savings.

Mistakes to avoid:

- Starting without a clear goal: It’s important to define a realistic goal for how much you want to save and the time needed to reach that goal.

- Mixing the emergency fund with other savings: Mixing your emergency fund with money intended for other purposes can make it difficult to track. Keep the fund separate.

- Not reviewing the fund regularly: Circumstances change, and you may need to adjust the value of your emergency fund. Don’t neglect to review it periodically.

7. Benefits of Having an Emergency Fund

Creating an emergency fund offers a range of benefits for your financial health. Having this reserve can be the difference that allows you to weather financial storms without jeopardizing your well-being.

Benefits of an emergency fund:

- Peace of mind: Knowing that you have a financial reserve for emergencies brings peace of mind and reduces stress.

- Prevention of debt: Having an emergency fund prevents you from resorting to loans or credit cards to cover unexpected expenses.

- Better financial control: By creating and maintaining an emergency fund, you are better prepared to handle any financial situation without harming your long-term goals.

Conclusion: The Importance of Having an Emergency Fund

Building an emergency fund is one of the smartest moves you can make to ensure your financial security. With it, you’ll be prepared to face unexpected events without the risk of falling into debt or compromising your financial stability.

By following the steps to create and maintain your emergency fund, you are building a solid foundation for your financial future. Remember that this fund should be a priority, and consistency in saving will be the key to reaching your goals. It doesn’t matter how much you can start saving with, what matters is that you start now and ensure you’re protected against life’s surprises.

Discover how to transform your relationship with money and finally achieve that long-awaited financial freedom. If you’ve ever felt overwhelmed by debt, disorganized budgets, and the sense that your money is simply vanishing, it’s time to take control.

In the e-book Master of Finances: How to Control Your Money and Achieve Financial Freedom, Ler mais renowned economist Tayrine Campos reveals practical, innovative strategies to help you:

- Analyze and effectively reorganize your financial situation;

- Create and maintain a realistic budget that truly works;

- Eliminate debt and invest with confidence;

- And most importantly, turn financial challenges into opportunities for a secure future.

This guide is perfect for anyone who wants to seize control of their finances, break free from the cycle of debt, and begin paving the way toward financial independence. If you’re ready to take the first step toward a worry-free financial life, check out this comprehensive and transformative guide:

Check out the Master of Finances e-book

Share this content:

Post Comment