Smart Consumption 3

big-ticket purchases, budgeting tips, buy now pay later, buying outright, cash flow, credit management, debt management, financial decisions, financial planning, financing options, installment loans, installment payments, interest rates, large purchases, managing debt, paying in installments, payment plans, pros and cons of installments, smart shopping, upfront payment

Tayrine Campos

7 months ago

0 Comments

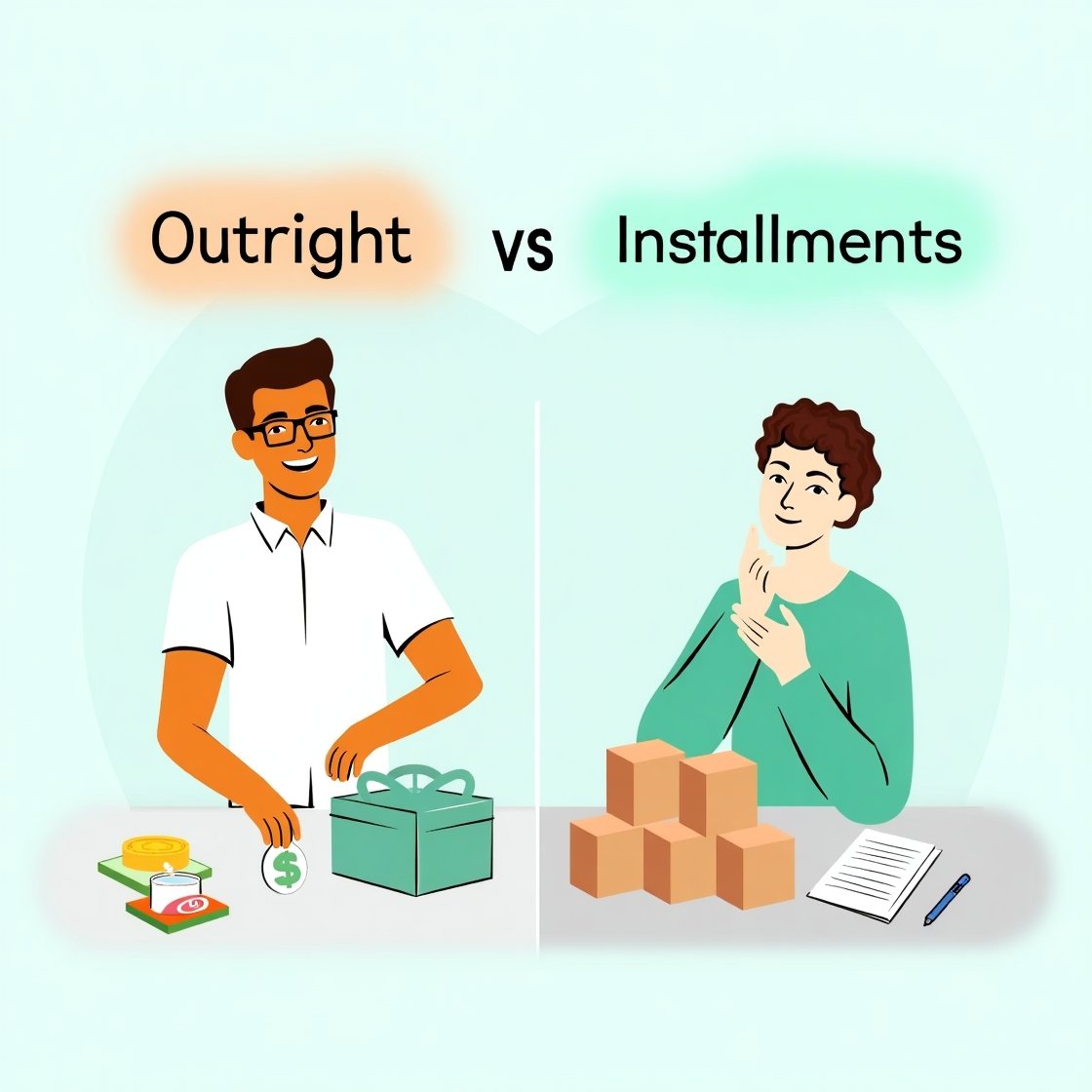

Buying Outright or in Installments: Which is the Best Option? 2025

When it comes to making big purchases, one of the most important decisions you’ll face is whether to buy outright or opt for an installment plan. From smartphones and furniture to cars and electronics, many consumers are faced with this question regularly. While both options have their advantages and disadvantages, understanding your financial situation, the costs involved, and how each option fits into your long-term goals is key to making the right choice. In this post, we’ll explore the pros and cons of buying outright versus buying in installments, helping you decide which is the best option for you.

What Does Buying Outright Mean?

Buying outright refers to paying the full price of an item or service upfront, without using any financing or installment plans. This means you’ll pay the total cost at the time of purchase, typically in a single transaction. Many people prefer this option because it means they own the product immediately, without owing any future payments.

What Are Installment Payments?

Installment payments, on the other hand, allow you to spread the cost of your purchase over a period of time. Rather than paying the full price upfront, you agree to make smaller payments at regular intervals (usually monthly) until the total price is paid off. This option is commonly used for big-ticket items like electronics, appliances, and even cars.

Installment plans often come with interest rates, although some offer 0% interest for a set period. Depending on the terms, installment payments can be a good way to afford expensive purchases, but they can also come with additional costs if the interest rate is high or if payments are missed.

Pros and Cons of Buying Outright

Let’s start by looking at the benefits and drawbacks of buying outright.

Pros:

- No Future Payments: When you buy outright, you pay once and own the item. There are no future financial obligations, and you won’t have to worry about missing payments or accumulating interest over time. This is ideal for those who want to avoid debt and keep their finances simple.

- Immediate Ownership: Once the payment is made, you own the product outright. There’s no need to worry about making monthly payments or dealing with the risk of repossession if you miss a payment.

- No Interest or Hidden Fees: Unlike installment plans, buying outright means you won’t be subject to any interest charges or hidden fees. What you see is what you get.

Cons:

- Large Upfront Cost: The main downside of buying outright is the large initial payment. If you don’t have the necessary funds saved up, this can be a significant barrier to making the purchase. For expensive items, paying the full amount upfront may not be feasible for everyone.

- Potentially Depleting Savings: If you need to use a significant portion of your savings to make the purchase, you may be left with less financial flexibility for other expenses or emergencies.

- Missed Opportunities for Investment: By paying outright, you forgo the opportunity to use that money for other investments that could potentially grow over time. Instead of tying up your funds in a purchase, you could invest that money elsewhere for a better return.

Pros and Cons of Buying in Installments

Now, let’s look at the advantages and disadvantages of choosing an installment plan.

Pros:

- Affordability: One of the biggest reasons people choose installment payments is affordability. Spreading the cost of a purchase over time makes it easier to manage, especially if the item is expensive. Monthly payments are often smaller and more manageable than paying the full amount upfront.

- Preserving Savings: With installment payments, you don’t need to use all your savings to make the purchase. This allows you to keep your emergency fund intact and avoid depleting your cash reserves.

- 0% Interest Offers: Some retailers and financial institutions offer installment plans with 0% interest for a specific period. If you qualify for such an offer and can pay off the balance before the interest rate kicks in, you can effectively make a purchase without paying any extra costs.

- Improved Cash Flow: Installment payments can help improve your cash flow management, particularly if you’re making a large purchase. This allows you to maintain a balance between your income and expenses while still getting what you need.

Cons:

- Interest Rates: The most significant downside of installment payments is the interest rates. Many plans come with interest charges, which can add a substantial amount to the total cost of the purchase. Over time, this can make the product much more expensive than it initially appeared.

- Long-Term Financial Commitment: With installment plans, you are committing to a series of future payments. This can impact your ability to make other purchases or save for future goals, as a portion of your monthly income is dedicated to the installment plan.

- Risk of Debt: If you’re not careful, using installment plans frequently can lead to debt accumulation. Missing payments or taking on too many installment plans can result in a negative impact on your credit score and finances.

- Ownership Delays: Depending on the terms of your installment agreement, you may not fully own the product until all payments are made. This means you could face restrictions if you want to sell or transfer the product before the balance is paid off.

Factors to Consider When Choosing Between Buying Outright or in Installments

Choosing the best option depends on your financial situation, goals, and the nature of the purchase. Consider the following factors before making your decision:

- Your Financial Situation: If you have the cash available and don’t want to take on debt, buying outright may be the best option. However, if your finances are tight, installment plans allow you to spread out the cost without emptying your savings.

- Interest Rates: If you’re opting for an installment plan, pay close attention to the interest rate. A high interest rate can significantly increase the cost of your purchase, so it’s best to avoid installment plans with high rates unless they offer 0% interest.

- The Purchase Amount: For smaller purchases, buying outright is usually a better option. However, for large-ticket items (like cars, furniture, or electronics), installment payments may be more manageable and practical.

- Your Future Financial Goals: Consider how an installment plan will affect your future finances. If you’re planning to make other large purchases or save for a goal, committing to an installment plan could impact your ability to do so.

- Length of Ownership: If you want immediate ownership and peace of mind, buying outright is the way to go. Installment plans may delay full ownership, so be sure you’re comfortable with that.

Conclusion: Which Option Is Best for You?

Ultimately, the decision between buying outright or in installments depends on your personal financial situation and goals. Buying outright is ideal if you can afford it and want to avoid debt or interest charges. On the other hand, installment plans can be a great way to make large purchases more affordable, but it’s important to be mindful of interest rates and long-term commitments.

Before making any purchase, carefully consider your budget, the total cost, and how the payment plan fits into your financial goals. Whether you choose to pay upfront or in installments, making informed decisions will help you manage your finances more effectively.

Discover how to transform your relationship with money and finally achieve that long-awaited financial freedom. If you’ve ever felt overwhelmed by debt, disorganized budgets, and the sense that your money is simply vanishing, it’s time to take control.

In the e-book Master of Finances: How to Control Your Money and Achieve Financial Freedom, Ler mais renowned economist Tayrine Campos reveals practical, innovative strategies to help you:

- Analyze and effectively reorganize your financial situation;

- Create and maintain a realistic budget that truly works;

- Eliminate debt and invest with confidence;

- And most importantly, turn financial challenges into opportunities for a secure future.

This guide is perfect for anyone who wants to seize control of their finances, break free from the cycle of debt, and begin paving the way toward financial independence. If you’re ready to take the first step toward a worry-free financial life, check out this comprehensive and transformative guide:

Check out the Master of Finances e-book

Share this content:

Post Comment